7 Common Conveyancing Problems in NZ and How to Solve Them

7 Common Conveyancing Pitfalls and How to Avoid Them

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal or financial advice. Property transactions involve significant financial commitments and legal obligations. We recommend seeking professional advice tailored to your specific circumstances before making any decisions.

Key Takeaways

- Due diligence steps like ordering a LIM are time-bound and require at least ten working days for council processing.

- KiwiSaver has become a massive funding source for first homes, with billions withdrawn annually, making timing and documentation critical.

- Fixed-fee conveyancing provides price certainty by including GST and standard disbursements in the initial quote.

- Unconsented works and title defects often surface late in the piece, requiring early investigation to prevent settlement delays.

- Standardised natural hazard disclosures in 2025 mean LIM reports now contain more detailed risk information than ever before.

The 2025 property market reflects a period of cautious confidence. According to data from the Real Estate Institute of New Zealand (REINZ), national residential sales counts increased 10.3% compared with 2024, reaching 80,655 sales. While the national median house price edged down slightly to $775,000, the steady volume of transactions means the legal "engine room" of these deals is busier than ever. In our experience, the primary danger in this environment involves letting avoidable legal or administrative issues derail a transaction at the last minute.

Conveyancing functions as the risk-management engine room of your property deal. It is where we identify and resolve problems before they become expensive mistakes. Whether you are buying a first home in Hamilton or selling a family residence in Christchurch, understanding the common hurdles can save you thousands of dollars and weeks of stress. We have seen these seven pitfalls trip up even the most prepared parties, but they are entirely manageable with the right approach.

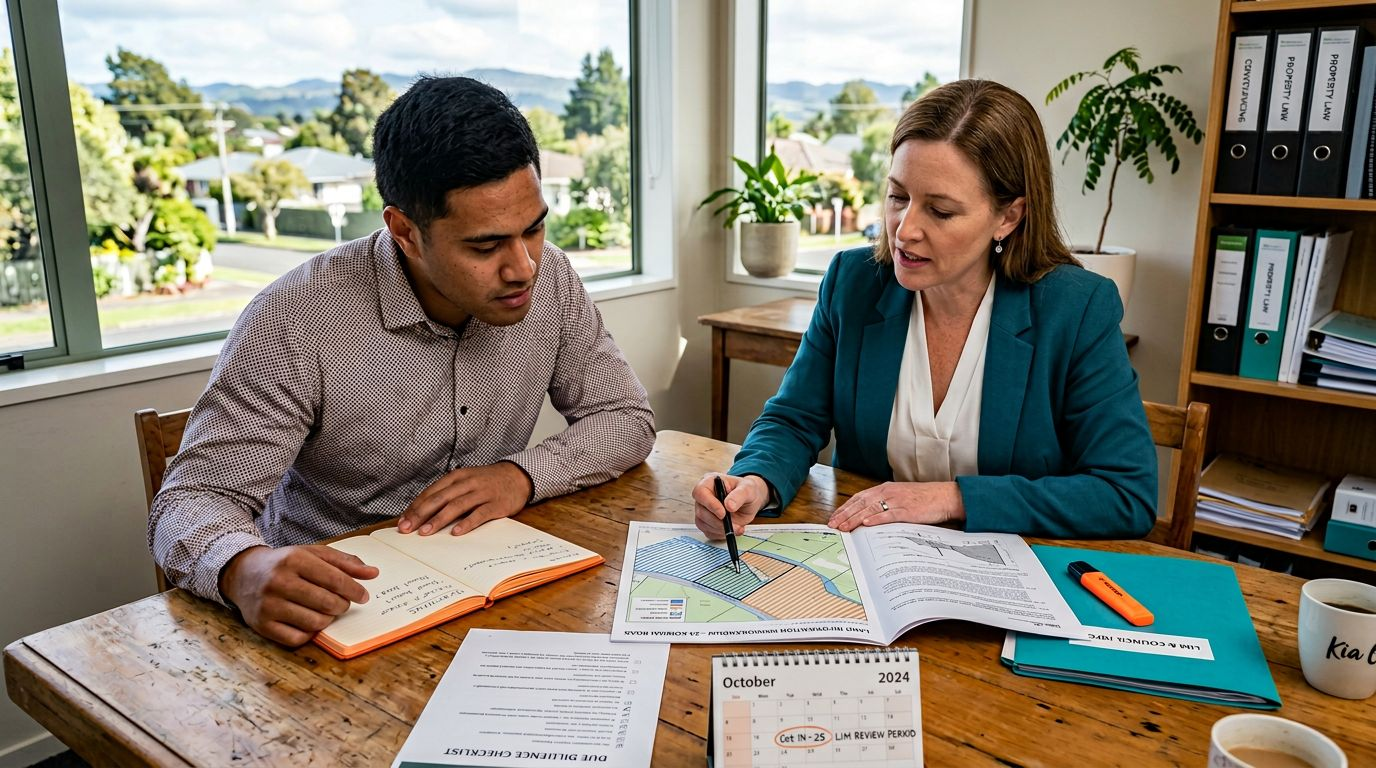

1. LIM and Natural Hazard Surprises

A Land Information Memorandum (LIM) is a comprehensive report issued by the local council that provides a summary of all the information they hold about a specific property. Under section 44A of the Local Government Official Information and Meetings Act 1987, councils must issue a LIM within 10 working days. We often see buyers leave this too late, failing to account for this statutory timeframe in their finance or due diligence conditions.

Recent regulations effective from 1 July and 17 October 2025 now require clearer, standardised natural-hazard disclosures. This means your LIM will likely be more information-dense regarding flooding risks or coastal erosion. In 2025, council fees for a standard residential LIM ranged from $290 in Christchurch to $563.50 in Wellington, while Auckland charged $375 for a standard request and $506 for an urgent one. Building these costs and timelines into your initial plan ensures you have the facts before your deposit becomes non-refundable.

2. Title and Easement Defects

The Record of Title is the legal proof of ownership, but it also contains "interests" that can restrict how you use the land. An easement, for example, might allow a neighbour to run a driveway across your property or give a utility company the right to access pipes under your lawn. A common mistake we observe is buyers assuming a "clear title" means no restrictions exist.

In our experience, identifying these defects early allows us to advise you on whether a shared driveway agreement is missing or if a restrictive covenant prevents you from building the shed you planned. We review these documents as part of our standard online property law services, ensuring you know exactly what you are buying into before you sign on the dotted line.

3. Unconsented Works and Illegal Additions

Many New Zealand homes have undergone renovations, but many of those changes lack the necessary building consents or Code Compliance Certificates (CCC). A CCC is the final sign-off from the council confirming that building work meets the building code. If a previous owner added a deck or converted a garage without permission, the liability often passes to the new owner.

We recommend checking the council property file against the physical layout of the house. If the kitchen has been moved or a load-bearing wall has disappeared but the council records show the original 1950s floor plan, you have a problem. Resolving these issues through a "Safe and Sanitary" report or a Certificate of Acceptance takes time, so spotting them early is vital.

4. KiwiSaver and Kāinga Ora Timing Issues

KiwiSaver acts as a central pillar of first-home funding for many New Zealanders. Data from Inland Revenue shows that as at 30 June 2025, $2.3 billion had been withdrawn from KiwiSaver for first-home purchases or financial hardship since 2015. This includes $1.9 billion specifically for first homes. In December 2025 alone, $196.3 million was withdrawn for first-home purchases.

The sheer volume of applications means delays are common. RNZ reports that there were over 58,000 hardship withdrawals in 2025, adding further pressure to the system. We've seen deals nearly collapse because a buyer didn't realise their provider required 10 to 15 working days to process a withdrawal. Our team manages these applications routinely, and you can find more detail in our full KiwiSaver first-home deposit guide. We receive the funds into our trust account and time them perfectly for settlement to avoid any last-minute panic.

5. Finance and Valuation Roadblocks

A "pre-approval" from a bank is a helpful starting point, but it usually comes with strings attached. The bank will often require a registered valuation of the specific property you are buying before they give the final "yes." If the valuation comes in lower than your offer price, you may need to find a larger cash deposit to bridge the gap.

We've seen this happen when buyers get caught up in a multi-offer situation and bid more than the market value. Ensuring your finance condition gives you enough time to get a valuation and bank sign-off is a key part of our risk management process. We work closely with your mortgage broker to ensure all bank requirements are met well before the settlement date.

6. Insurance Complications

Obtaining house insurance has become more complex in recent years, particularly in areas prone to natural hazards. Banks will not settle a mortgage unless they have proof of insurance that is "held covered" from the day of settlement. If a property has a history of EQC claims or sits in a flood zone identified in the 2025 natural-hazard disclosures, some insurers may decline cover or charge a significant premium.

We advise all our clients to check insurance availability as their very first step. If you can't get insurance, you can't get a mortgage, and the deal cannot proceed. We handle the legal side of EQC claim transfers, which usually incurs a small add-on fee of $150.00, to ensure your interests are protected if there is ongoing damage to be repaired.

7\. Settlement Day Logistics

Settlement day is when the money moves and the keys are handed over, but it requires precise coordination. A common pitfall is the "domino effect," where a delay in one person's sale prevents them from buying their next home, holding up an entire chain of buyers and sellers. We've seen this happen when people try to move house on a Friday afternoon, leaving very little time to resolve banking glitches before the weekend.

Conducting your final pre-settlement inspection at least two working days before the big day allows time to address any issues, such as the seller leaving rubbish behind or a newly broken window. Our role is to coordinate with the other party's lawyer and the banks to ensure the money moves as early as possible on the day.

Transparent Costs for Peace of Mind

One of the biggest stresses in any property deal is the fear of hidden legal costs. We believe in providing clear, upfront pricing so you can budget with confidence. Our fees are all-inclusive of GST and standard disbursements, and we typically take them from the final settlement sum so you don't have to pay upfront.

Our standard transparent, fixed conveyancing fees from $1,499 (selling) and $1,799 (buying) cover the essential legal work. For more complex deals, we use a simple add-on menu:

- KiwiSaver funds withdrawal: +$300.00

- Kāinga Ora First Home Grant: +$100.00

- Mortgage facility (per facility): +$150.00

- Unit title sale or purchase: +$150.00

- Trust involvement: +$200.00

- Drafting a Sale and Purchase Agreement: +$150.00

By choosing a fixed-fee service, you remove the risk of an escalating hourly bill if a minor issue arises. Our goal is to make the process as straightforward as possible, using our experience to spot those seven pitfalls before they become problems. If you are ready to move forward with your next property move, our nationwide online property law service is here to manage the transaction from start to finish, keeping you updated every step of the way.